“The bitterness of poor quality remains long after the sweetness of low price is forgotten.” — Benjamin Franklin (US Founding Father)

People at home insurance hunt are typically looking for the cheapest one. While saving money is important, choosing a policy based solely on price can leave you exposed to costly surprises when you need coverage the most.

Rising property values and increasingly frequent weather-related claims have made home insurance more important than ever. Yet policies that appear similar at first glance can differ significantly in cost, coverage limits, exclusions, and claim protections. Comparing quotes before making a decision helps ensure you’re not only getting a competitive rate but also the protection your home truly needs. Whether you are purchasing a new policy or reviewing an existing one, you can start by exploring homeowner insurance NJ options for your property to find comprehensive coverage tailored to your home’s unique risks and protection needs.

Here are five reasons why taking the time to compare insurance quotes is one of the smartest financial decisions a homeowner can make.

KEY TAKEAWAYS

- Home insurance premiums can vary significantly between insurers, even for similar coverage.

- Comparing quotes helps uncover important differences in coverage limits, exclusions, and endorsements.

- Regularly reviewing policies ensures your coverage keeps pace with changes to your home and lifestyle.

- Bundled insurance packages are not always the most affordable option and should be compared against alternatives.

1. Prices for the Same Coverage Vary Significantly

Insurance providers assess risk differently, which means two companies can offer dramatically different premiums for nearly identical coverage. Two policies that look identical on the surface can carry price differences of hundreds of dollars per year. That gap isn’t random. It reflects how each insurer weighs factors like:

- Your postal code

- Age of your roof

- Your claims history

- The construction type of your home

Most homeowners who have never compared quotes assume their current rate is roughly in line with the market. Often it isn’t, and the only way to know is to actually look at what else is available for the same coverage level.

2. Compare Quotes to Know What You’re Actually Getting

A low premium may look attractive, but the true value of a policy lies in its coverage details. Two quotes at similar price points can differ significantly in how they handle things like water damage, sewer backup, detached structures, or personal liability. These distinctions aren’t always obvious from a summary page, and they tend to matter a great deal at claim time.

Taking the time to find the best home insurance quotes with iSure allows you to compare not just premiums but the actual coverage terms side by side, which is the only way to make a genuinely informed decision. Insurance brokers work with multiple insurers, allowing you to compare options in one place instead of contacting each company separately and trying to understand different policy formats on your own. That clarity can make the insurance-buying process much easier and more effective.

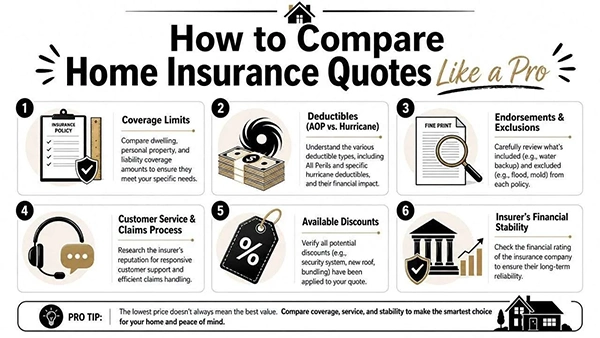

Here’s a simple checklist for comparing quotes:

3. Your Home’s Risk Profile Changes Over Time

A policy that was right for your home five years ago may not reflect your current situation accurately. Renovations, a new roof, a finished basement, a home office, or even a trampoline in the backyard can all change how insurers assess your risk and what coverage you actually need. Many homeowners renew their policy every year without reviewing whether the coverage still fits, which means they may be underinsured for improvements they’ve made or paying for coverage that no longer applies.

Comparing quotes at renewal is a good habit precisely because it forces a fresh look at what the policy covers against what the home actually needs. Insurers update their offerings regularly, and the product that best fits your situation today may not be the same one you signed up with originally.

4. Bundling and Discounts Don’t Always Deliver the Savings They Promise

Many insurers offer discounts for bundling home and auto coverage, and those discounts are real. But a bundled price from one insurer isn’t always lower than two separate policies from two different providers. The bundling discount sometimes makes a more expensive baseline policy seem like a better deal than it actually is when compared to the market.

According to an article by the Insurance Bureau of Canada, homeowners can save on premiums by shopping around at renewal. Many homeowners assume their loyalty discount or bundle savings represent the best available rate. But it’s not always so. Compare quotes to verify whether the bundled deal you’re being offered is genuinely competitive or just discounted relative to a higher starting point.

5. Claims Record and Coverage Gaps Can Hit You Later

The policy you choose today can have long-term implications beyond your immediate coverage needs. Policies with low coverage limits or significant exclusions can leave gaps that result in out-of-pocket losses, and depending on how a claim is handled, those gaps can show up on your insurance record in ways that affect what you’re offered in the future.

In practice, understanding what a policy won’t cover before you buy it is just as important as understanding what it will. A gap in sewer backup coverage, for example, is easy to overlook when reading a summary but becomes very consequential when a basement floods. Comparing policies carefully is the most reliable way to find those gaps.

Conclusion

Home insurance is designed to protect one of your most valuable assets, making it too important to choose based on convenience alone. The consequences of getting it wrong are real and sometimes exorbitant. Comparing quotes before committing doesn’t require expertise or hours of research. It just requires looking at more than one option before deciding. For something that protects your biggest asset, that extra step is worth taking every single time.

So take the time to compare options, and consider speaking with your insurance representative about ways to reduce your current policy premiums.

FAQs

How many home insurance quotes should I compare?

At least 3-5 quotes. This provides a broader view of pricing, coverage options, and available discounts.

Is the cheapest insurance policy always the best choice?

Not necessarily. Lower-priced policies may include lower coverage limits, higher deductibles, or exclusions that could leave you financially exposed during a claim.

How often should I compare home insurance quotes?

It’s wise to compare quotes at every renewal period or whenever significant changes occur, such as renovations, home additions, or major purchases.

Can switching insurers affect my coverage?

Yes. Different insurers offer different coverage options and endorsements. Always review policy details carefully to ensure you’re maintaining or improving your level of protection.

Do insurance brokers charge extra for quote comparisons?

In many cases, brokers are compensated by insurance providers rather than directly by homeowners. They can often help compare multiple options without additional upfront costs.